The rise in prices for CPUs, GPUs, DRAM memory, and flash storage have counterbalanced the imbalance between supply and demand such that the overall server market had only a slight sequential decline in the first quarter of 2026. This is not only amazing, but perhaps also intentional on the part of the OEMs and ODMs that bend metal around components to make servers.

If you were in the place of the OEMs and ODMs, you would be passing on the increasing costs of these components, and then given that supply exceeds demand by maybe 25 percent to 30 percent (based on hints from the big OEMs), you might even engage in a little opportunistic price increases where contracts with customers have not locked in the cost of machines. Considering how hard these server manufacturers work, and for the most demanding and penny-pinching customers in the world, they deserve a little margin and we hope that for once they are getting a little vig.

In the first quarter of 2026 according to the market researchers at IDC, the world consumed $122.62 billion in servers, up 30.4 percent year on year but down 2.1 percent sequentially. This is nothing compared to the historical sequential decline from the fourth quarter to the following first quarter that the server market has had in the decades before the GenAI boom. Everybody in the world knew the fourth quarter was when IT budgets were being set for the following year, and if IT shops didn’t spend all of their budget, it would not be held pat or raised in the next year. So Q4 was always stronger that Q3 and Q2 was always stronger than Q1 and usually bigger than Q3. There is a sawtooth pattern there, which is affected by the server roadmaps of CPU and system makers.

These days, at least for the past several quarters, there seems to be a new normal level of server spending despite all of these puts and takes, as they say on Wall Street.

Here is what the quarterly server revenue situation looks since 1999, with a gap in the IDC data shown in the blue line:

If you inflation adjusted this data, which I need to do, it would make the spending way in the past look bigger than it is. But not enough to diminish the exponential explosion caused by the GenAI wave, which is now being met by a massive, global refresh cycle for non-AI systems at exactly the time that all of those components are seeing prices rise dramatically because there is too much demand and not enough supply.

According to IDC, the world spent $68.9 billion on GPU-accelerated servers in Q1 2026, up 24.8 percent but down 2.5 percent sequentially. Again, I think price increases nearly compensated for shipment declines due to component shortages. No one thinks this is a demand problem at all, including me. GPU systems represented 56.2 percent of overall server revenues, which is astounding until you consider that a datacenter GPU accelerator with its HBM memory costs like $50,000 these days, and will soon be close to $100,000 if not more with next generation of multi-chip devices.

Interestingly, IDC broke out revenues for other XPU-accelerated machines for the first time in its publicly available data, which is a juicy bit of news. In Q1, there were $17.1 billion in XPU systems sold – I think mostly based on Google TPUs and Amazon Web Services Trainiums with a smattering of others from Microsoft, Cerebras Systems, Groq, and a handful of others. These XPU systems accounted for 13.9 percent of server revenues, up from 8.2 percent a year ago and nearly nothing a few years before that.

Add them up, and GPU systems plus XPU systems accounted for $86 billion in revenues, comprising 70.2 percent of overall server revenues. Yup, that’s not a typo. That’s up from 62.2 percent of overall server revenues in the year ago period.

The age of X86 dominance is almost over if you count all of the money in the systems that use them. X86 hosts drove $63.9 percent of sales, down 2.9 percent year on year and down 8.5 percent sequentially. If components were not so expensive and in such short supply, it is likely that the X86 server business would have grown dramatically in the first quarter.

Non-X86 machines, dominated by the homegrown Arm processors created by the hyperscalers and cloud builders as well as Nvidia systems based on its “Grace” Arm server CPU, pushed $58.7 billion in gear, up by a factor of 2.1X year on year and up 5.8 percent sequentially.

X86 systems had 52.1 percent revenue share in Q1 2026, while non-X86 machines had 47.1 percent share. IBM’s Power Systems RISC machines and System z mainframes accounted for a slice of this non-X86 business, so don’t think that it is all Arm gear. It won’t be too long before we have RISC-V machines on the rise, too. . . .

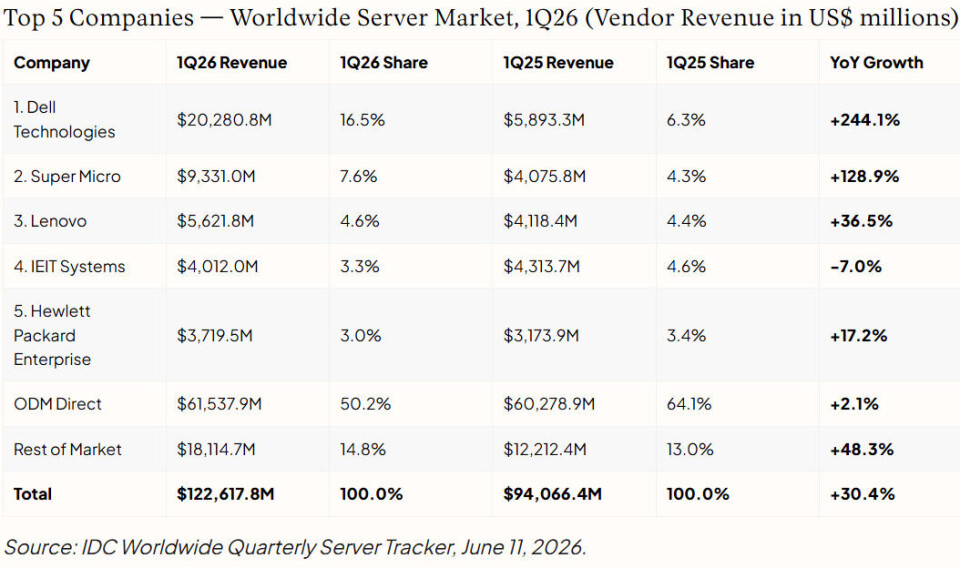

Here is how the vendor breakdown looked in Q1 2026:

Dell, having been anointed the chosen OEM by Nvidia, is benefitting mightily from its status, and not just because of its enterprise customers but because of some big sovereign, neocloud, and model builder deals it has taken down. As we showed in our recent financial coverage of Dell and HPE, Dell’s AI server business is an order of magnitude larger than that of HPE, which is why Dell’s overall server business is 5.5X bigger than HPE’s is.

The ODMs that serve the hyperscalers and cloud builders are humming along, constrained only by component supplies. Their business would be much larger if all of that chippery was not so hard to get their hands on.