Google

might have come late to the cloud game and it might be a distant third compared

to Amazon Web Services and Microsoft Azure, but Google Cloud is making up for

lost time thanks to the killer app that GenAI has become. And while Nvidia is

the dominant full stack player out there when it comes to hardware, which is

why its revenues and profits have exploded, Nvidia’s Nemotron models are not anywhere

as popular as Google Gemini, OpenAI GPT, or Anthropic Claude.

Here’s

the funny bit. Google never really believed in raw infrastructure clouds. The original

cloud services from Google – Compute Engine and App Engine – abstracted all of

that infrastructure away to make infrastructure easier, invisible. More like

the Borg and Omega platform that internal Google programmers had access to. And

customers didn’t care.

But

here we are, more than a decade later, and IT organizations have learned to stop

hugging their physical and virtual servers and they are perfectly happy to use

APIs for Google’s Gemini model as well as to train their models and run their

inference against Google’s vast global fleet of GPUs and TPUs. Which is why Google

Cloud is growing faster than either AWS or Azure in the first quarter. The customers

have finally caught up to the Google vision, and there are customers who are

choosing the full Google stack for the GenAI, from the raw iron up through data

services and inference engines.

Building

a cloud has not been easy for Google, and it lost a lot of money on it in the

early years, as the chart above shows. But now, Google Cloud is as large as all

of Google was a decade ago – and Google Cloud is more profitable by a factor of

1.25X compared to the entirety of Google was back then. It is arguable that

Google is the best company in the history of IT in terms of building hyperscale

infrastructure and running it efficiently, and that is showing up in the

operating income for Google Cloud. It just took a bit of time for Google to get

there and for IT shops to catch up to the culture that the search engine and

advertising giant was peddling.

The

bad news if you are a competitor of Google’s is that the search engine business

and the various other advertising businesses at the company (YouTube and

network advertising) are collectively doing well. Search revenues were up 19

percent to $60.4 billion, YouTube advertising was up 11 percent to $9.9

billion, while network advertising was off 4 percent to $7 billion. The

subscriptions, platforms, and devices business, which includes Pixel phones,

YouTube Music, Google One, and other services, rose by 19 percent to $12.4

billion. So, despite all the grief that comes as we use chattybots to do

searches, these businesses are still growing, and growing faster than you might

think possible.

It

is not clear how many subscribers Google has for its flagship Gemini model, but

the company did say that its “first party models” – meaning its own Gemini models

served out as APIs, as well as Lyria, Nano Banana, Veo, and Gemma – processed

an average of 16 billion tokens per minute in the March quarter, up 60 percent from

10 billion tokens per minute in the Q4 2025 quarter. By our math and what

Google said about its averages, that means it processed 917.3 trillion tokens against

Gemini on behalf of customers in Q3 2025, with 1,310.4 trillion tokens in Q4

2025 and 2,050.6 trillion tokens in Q1 2026.

Presumably

the Google Gemini App division pays Google Cloud for the use of TPUs, just like

any other customer does. (Albeit at an attractive price, I suspect.) Google does

not talk about how many tokens it is generating for customers using Nvidia or

AMD GPUs. But Sundar Pichai, the company’s chief executive officer, said on a

call with Wall Street analysts that in the past twelve months, 330 customers on

Google cloud had processed over 1 trillion tokens each, and 35 of these had

broken through the 10 trillion token barrier. The use of the BigQuery tabular

database in conjunction with Gemini has grown by 30X in the past year as well

as companies see the benefits of a completely unified Google AI stack, from TPU

up through Gemini and the

Gemini Enterprise Agent Platform (an enhanced version of what was formerly known

as Vertex AI) that wraps around it.

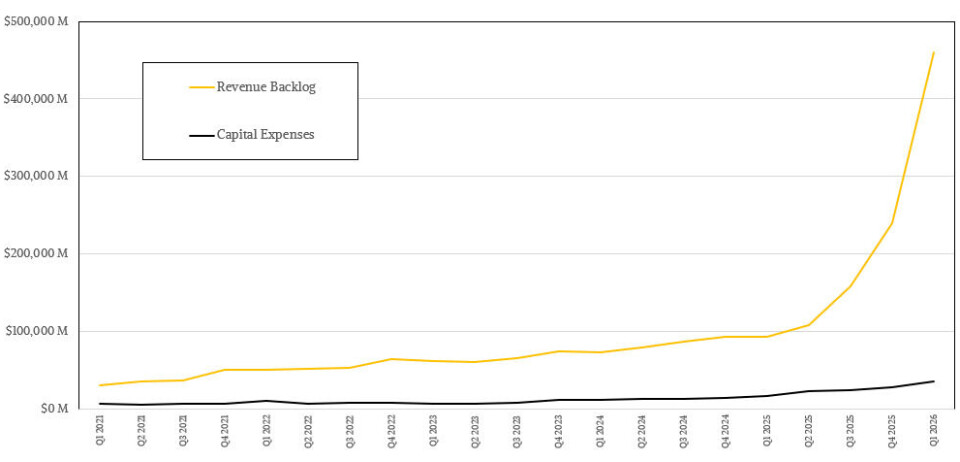

This

is the driving force for the phenomenal growth that Google saw in its eponymous

cloud in the first quarter, and its enormous revenue backlog of $462 billion – about

half of which will be recognized within the next two years – is why Wall Street

did not freak out when Google talked about spending somewhere between $180

million and $190 million this year on capital expenses. The lack of such a

revenue backlog is why Meta Platforms took a shellacking when it was going to

spend on that order of magnitude.

As

you can see, the capex has to rise to keep pace with the backlog, which is not

dominated by model builder OpenAI, whose revenue streams and operating losses

are something to worry about when you are planning three, four, or five years

into the future.

Google

Cloud is finally hitting its stride, and I think part of the reason is that

full stack integration. So does the company’s CEO.

“Google

Cloud is differentiated because we are the only provider to offer first party

solutions across the entire enterprise AI stack,” Pichai said on the call. “Our

growth in revenue, operating margin, and backlog highlights this

differentiation. Our Enterprise AI solutions have become our primary growth

driver for Cloud for the first time. In Q1, revenue from products built on our

gen AI models grew nearly 800 percent year over year. We are winning new

customers faster, with new customer acquisition doubling compared to the same

period last year. We are seeing strong deal momentum, doubling the number of

$100 million to $1 billion deals year on year, and signing multiple billion

dollar plus deals. And we are deepening relationships with existing customers.

Customers outpaced their initial commitments by 45 percent, accelerating over

last quarter.”

To

put the numbers on it, Google Cloud had revenues of just a tad over $20 billion,

up 63.4 percent year on year and up 13.4 percent sequentially. (That is more

than double the

growth of Amazon Web Services in the same Q1, but AWS is almost twice as

large as Google Cloud.) If current growth rates persist, Google Cloud would

catch AWS, with each having more than $82 billion in revenues by Q1 2029.

Google can certainly afford to invest to underpin that level of cloud revenue.

But as I said higher up in this story, the important thing is that Google Cloud

is showing better profitability, with operating income up by more than a factor

of 3X year on year to $6.6 billion, which was up 24.2 percent sequentially. Some

prior investments in infrastructure are clearly paying off.

As Q1 2026 came to an end, Google had shelled out

$35.67 billion in capital expenses, and the company said that about 60 percent

was for servers and 40 percent was for networking and datacenters. This ratio

has held for the past five quarters that Google has been talking about it.