We

are all full aware of what the hyperscalers, cloud builders, and AI model

builders are all doing to build out their datacenter infrastructure to support

their AI aspirations. But it is hard to get a sense of what regular enterprises,

service providers, governments, academic institutions, neoclouds, and sovereigns

– who will eventually represent maybe half of total AI spending – are doing. So

we have to use the sales of the traditional original equipment manufacturers as

a kind of proxy.

Depending

on the OEM, there are a fair amount of sales of chips or systems to

hyperscalers and cloud builders in the mix. IBM has basically none, Hewlett

Packard Enterprise, Dell, and Lenovo quite a bit more, and Supermico has most

of its sales to handful of very large companies and is more like an ODM. Cisco

Systems is somewhere in the middle, selling plenty of AI stuff to hyperscalers

and cloud builders but also selling AI wares into its vast UCS system customer

base, which numbers 90,000 unique customers worldwide after 17 years of being a

system OEM.

Teasing

out hyperscaler and cloud builder sales is tricky, and not the least of which

because Cisco sells both chips and optics to customers that build their own

systems as well as complete systems for those who don’t want to do that because

they are not at a sufficient scale for that to make sense.

Let’s

pick apart the Cisco numbers for the third quarter of fiscal 2026 just the same.

In

the quarter ended in April, Cisco’s overall revenues were $15.84 billion, up 12

percent year on year. Operating income rose by 23.7 percent to $3.96 billion,

and net income was up 35.4 percent to $3.37 billion. Like everyone else in the

world, Cisco wants to cut its overhead costs, and it is using AI as an excuse

to do layoffs. We have our doubts how much this reduction of around 4,000

people from Cisco’s workforce has to do with AI. It seems like every company is

looking to trim their coronavirus pandemic fat in human resources, and AI

provides air cover to do so as well as an impetus for retained employees to

figure out ways to make AI useful real quick now. . . .

In

early 2024, Cisco had about 85,000 employees and has reduced its headcount by

13,750 people in four rounds of layoffs over the past year and a half. (One

round was very small, at about 150 people.)

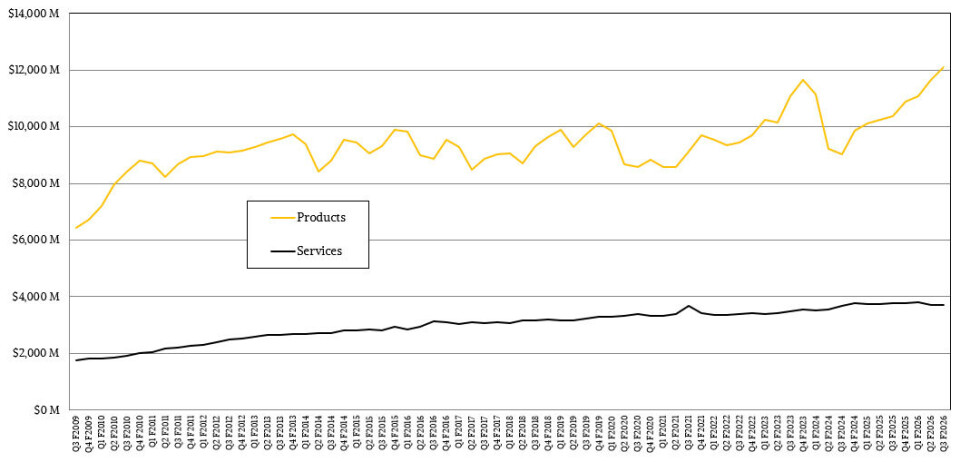

Cisco

is still largely a product peddler, but services is creeping up ever so slowly

to have a slightly larger share of the revenue pie at the company. But don’t get

too excited – the change to services revenue streams is relatively glacial,

from around 20 percent way back in 2009 (when we first started tracking the

company’s finances) to just under 25 percent in the trailing twelve months.

Some of that is due to Cisco being successful selling merchant switch and

router ASICs to hyperscalers and cloud builders as well as its Acacia optical transceivers.

It isn’t so much that services is not growing, but rather product sales have

just hooked an exponential curve.

As

the third quarter came to a close, Cisco had a revenue backlog of $43.5

billion, essentially unchanged from Q2 F2026, and it had $16.64 billion of cash

and equivalents in the bank.

Like

other OEMs, Cisco likes to talk about AI orders but not AI revenues. (Well, IBM

actually just stopped talking about even AI orders, and probably because it is

mostly a services play for Big Blue unless it starts counting Power Systems and

Z mainframe revenues as AI just because its processors have native matrix math

accelerators.)

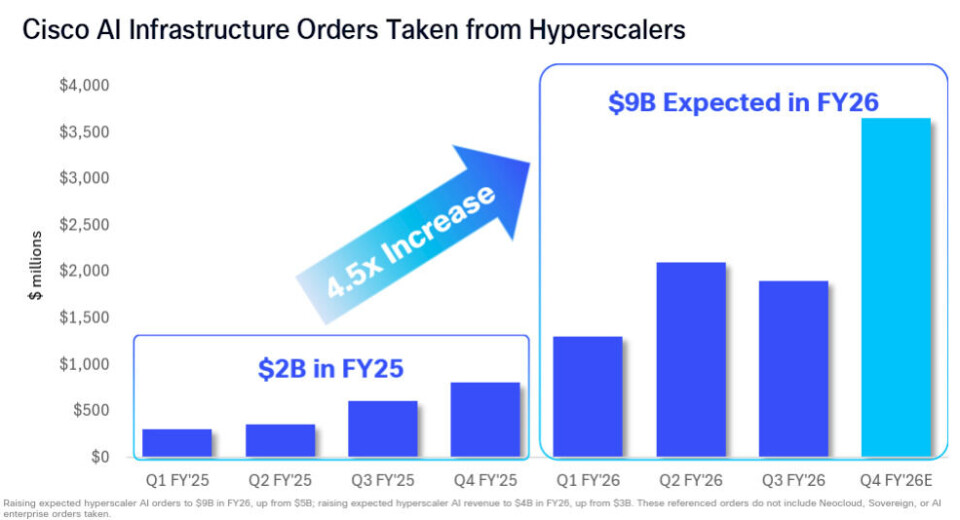

Here

is a handy chart that Cisco made showing its to hyperscalers, by which Cisco

means hyperscalers and cloud builders as we use these terms here at The Next

Platform. Take a gander:

As

fiscal 2026 was getting going, Cisco was projecting that it would have north of

$5 billion in AI orders from hyperscalers and cloud builders this fiscal year,

and this is now being updated to $9 billion. If you do the math on that, this implies

that Cisco will book $3.7 billion in AI orders to hyperscalers and cloud

builders in its fourth quarter of fiscal 2026 ending in July.

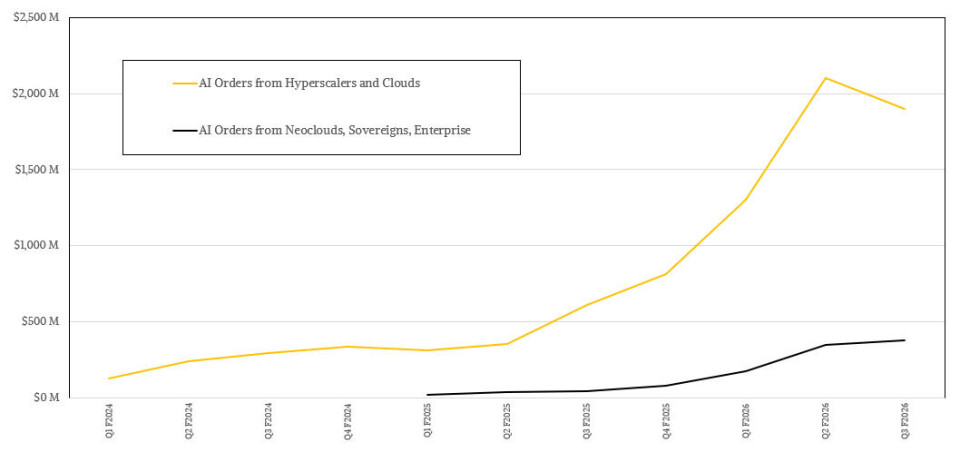

In

the third quarter, AI product orders to hyperscalers and cloud builders were up

by 2.1X to $1.9 billion. Product orders by other customers were up a more

subdued 19 percent, but that is nothing to cry about. All told, product orders

rose by 35 percent year on year. Enterprise orders were up 18 percent, public

sector orders rose by 27 percent, with service providers more than doubling while

telcos were up 9 percent. Telcos are only just beginning to catch the AI wave,

apparently.

Of

these $9 billion in AI orders, Chuck Robbins, Cisco’s chief executive officer,

said about $4 billion of that will be recognized in the current fiscal year,

and added later in the call with Wall Street that it should recognize at least

$6 billion in AI revenues from hyperscalers. The Acacia pluggable optical

transceiver business had over $1 billion in orders and is on track to triple

its order book this year, and added that Cisco has shipped over 750,000 400

Gb/sec units and over 40,000 800 Gb/sec units, which he said exceeds the shipment

levels of the next biggest supplier. (Wouldn’t it be funny if some hyperscalers

and cloud builders want to use Cisco transceivers with Arista Networks or

Nvidia switches?)

On

the Silicon One P200 front for scale across networks linking together AI

datacenters, Robbins said that Cisco has five design wins with hyperscalers

and cloud builders.

Robbins

said that Cisco had $300 million in AI infrastructure orders – servers,

switches, and such – from neocloud, sovereign, and enterprise customers in the

third quarter, with triple digit growth in all three quarters so far this

fiscal year, with a pipeline of $3 billion. In my model, AI system orders were

up 112 percent to $880 million, and Acacia optics orders rose by 5.4X to just a

tad over $1 billion. Add it all up, and Cisco had $2.2 billion in orders for AI

stuff in Q3 2026.

Enterprise

datacenter switching orders – Nexus switchery – was up by more than 40 percent,

and have grown by double digits in the past seven of nine quarters. Two years

ago, the GenAI boom started to hit enterprise customers, forcing them to

carefully consider the front end networks and systems that will feed into AI

systems. Campus and branch networks are also going to feel the heat from AI

workloads, and Cisco just did a survey of 3,500 IT people responsible for the

networks at their companies and 93 percent say they don’t just have to upgrade

the front end networks linking their enterprise platforms, they are going to

have to upgrade campus and branch networks, too.

It

is important to remember that some of this growth is for price changes as the

costs of GPU accelerators, CPUs, DRAM memory, and flash storage have gone

bonkers in recent months. To give a hint about how this helps Cisco’s numbers,

Mark Patterson, Cisco’s chief financial officer, said on the call with Wall Street

that outside of the hyperscalers and cloud builders, order growth was 10

percent in Q2 and 19 percent in Q3. Of that incremental sequential 9 percent

growth in business, about half came from increased shipments and the other half

came from price increases.

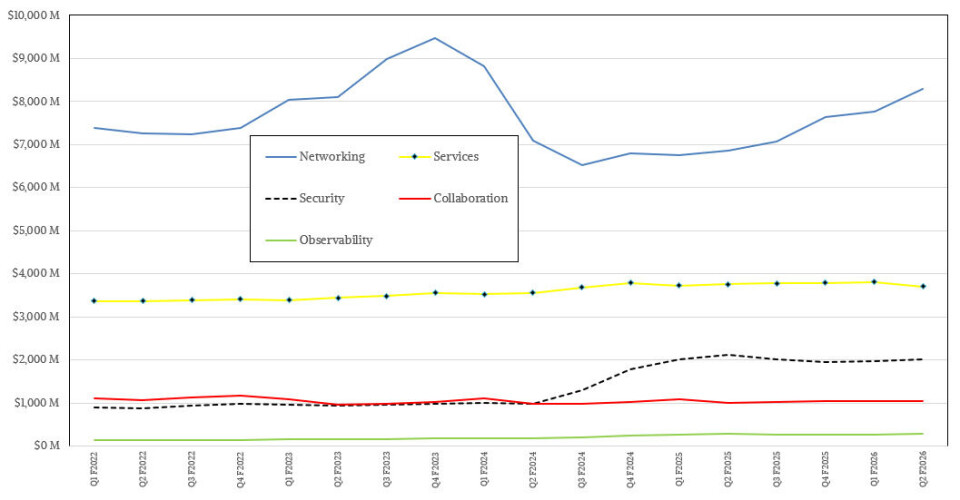

The

Networking group, which has servers, switches, and routers as well as merchant

silicon and optics all mashed up, had $8.82 billion in sales up 24.7 percent

year on year. I know this other stuff is important to Cisco customers, but it either

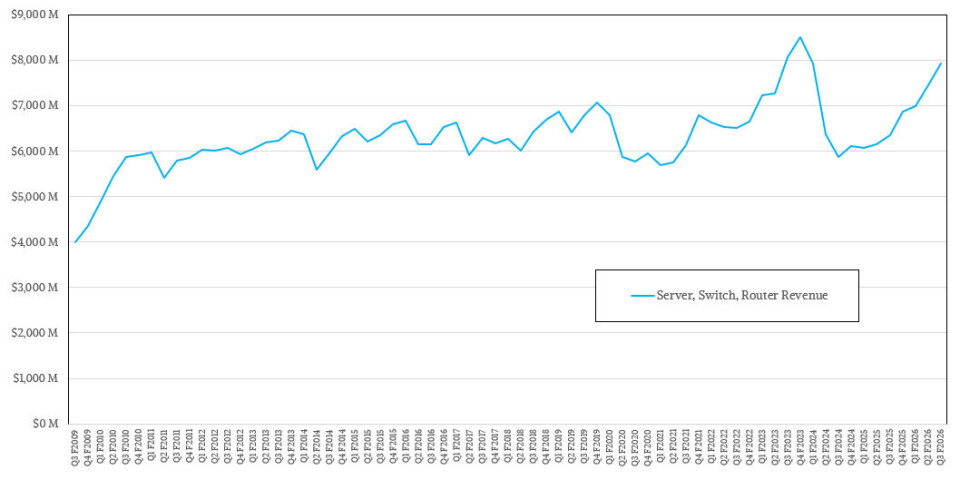

lives outside of the datacenter or far above in the stack.

As always, we try to figure out what the “real” Cisco

datacenter business is, extracting out campus and branch networking and other

things in the Networking group that are outside the glass house. (More of a

steel warehouse these days, really.) My model suggests that this real

datacenter business at Cisco weighs in at $7.93 billion in Q3 2026 and had

$1.96 billion in operating income, about 24.7 percent of sales. This is a very

respectable datacenter platform business, and there is no reason to believe it

will not get bigger.