Like

so many other IT suppliers to the tech titans, it will not be long before AI

networking will be the largest part of the business at Arista Networks. In

fact, if the company can get more supplies of switch ASICs and other

components, it could happen this year. If not, the cross over with the core

datacenter networking business that has defined the company in its first decade

and a half will be eclipsed by AI networking for scale up, scale out, and scale

across fabrics in 2027 for sure.

Given

the shortages in the IT industry for all kinds of components, Arista has

visibility into its hyperscaler and cloud builder customers, and not because

these customers are generous with their capacity planning, but because if they aren’t

honest about what they need a year early, Arista can’t get the components scheduled

and the gear built.

We

don’t know what the supply constraints are for the Arista products, but we do

think it is telling that Arista raised its guidance for 2026 from $11.25

billion to $11.5 billion and its for AI-related networking from $3.25 billion

to $3.5 billion when talking about its first quarter results ended in March. That

is another way of saying that the rest of the business is stuck in the mud.

Which is why Wall Street was not happy with Arista when the numbers came out.

To

get a better picture of where Arista is going and where it has been, we put

together this summary by product category a few quarters ago, and we have

updated it with the most recent guidance:

And

here is the raw data behind that chart:

Here’s

the thing, though. Arista has actually turned in good numbers, and it is positioned

to benefit mightily from the GenAI boom, particularly as it moves from

supplying scale out Ethernet fabrics to supporting the ESUN scale up protocol

on switches beginning in 2027 as well as scale across Ethernet fabrics that

glue datacenters together for very large scale AI systems, which the company

can sell now.

Jayshree

Ullal, Arista’s chief executive officer, explained that opportunity on the call

with Wall Street analysts thus:

“The

advent of ESUN, Ethernet for Scale-Up Networking, specifications allows for

increasing or decreasing computing power in a flexible manner with Ethernet to

automatically adapt to workload demands. Scale up will be a new entry for

Arista in 2027 and beyond, where we will be working closely with our customers

to build AI racks with very fast interconnects for co-packaged copper, CPC, or

open co-packaged optics, CPO, as well as supporting collectives and memory

acceleration.”

“Scale-out

or horizontal scaling involves adding more machines to a leaf/spine fabric,

moving workloads across multiple servers or nodes or even connecting other

elements like storage or CPUs. As you scale out massive datasets, bottlenecks

can be resolved with collective and protocol acceleration at L2, L3, and cluster

load balancing, all at wire rate. The system must deliver consistent

performance without degradation as more nodes participate. Arista is a shining

example here with greater than a hundred cumulative customers to date in 800 Gb/sec

Ethernet deployments, and we expect the addition of 1.6 Tb/sec in 2027 at

production scale.”

As

for scale up and scale across network sales, Ullal did not make any specific

predictions, but she did say that in the mid-term, scale across would drive at

least a third of the company’s AI sales to two thirds for normal scale across

Ethernet networking. She offered no guidance on ESUN scale up switch sales on

top of that, and said that was really going to not be material until 2027 and

into 2028. Ullal did say that the majority of customers getting ready for early

trials are waiting for 1.6 Tb/sec ports, but a few customers are experimenting

with ESUN atop 800 Gb/sec gear.

As

for the supply chain issue that is governing Arista’s sales to a large extent,

Ullal said that it started out with a DRAM problem that might be a few

quarters, and now it is a wafer and package fabrication problem that is

affecting the whole chip industry and it may take one or two years to

normalize. Hence the rise in purchase commitments at Arista, which we presume

customers are prepaying with deferred revenues, also double compared to this

time last year, to help cover those costs and lock in prices now as best can be

done.

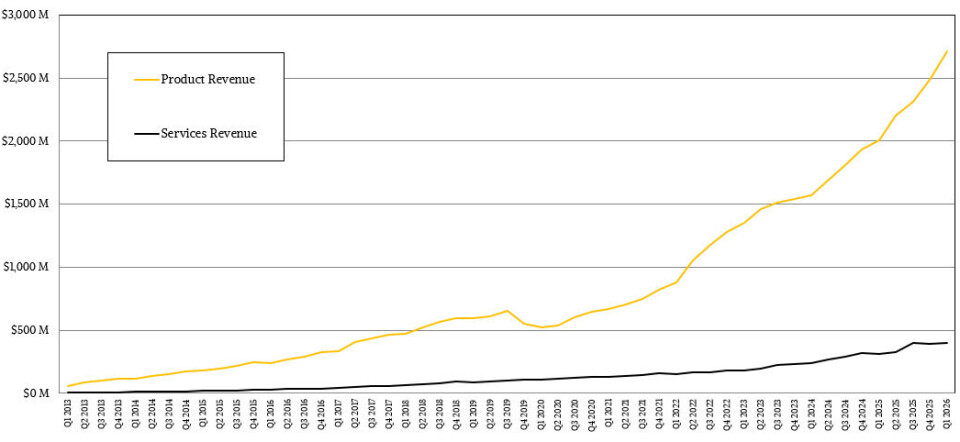

In

the March quarter, Arista had $2.31 billion in product revenues, up 36.6

percent year on year and up 10.3 percent sequentially. That is a pretty good

first quarter for any IT supplier in terms of growth. Services revenues rose by

27.3 percent to $397.7 million, up a smidgen sequentially.

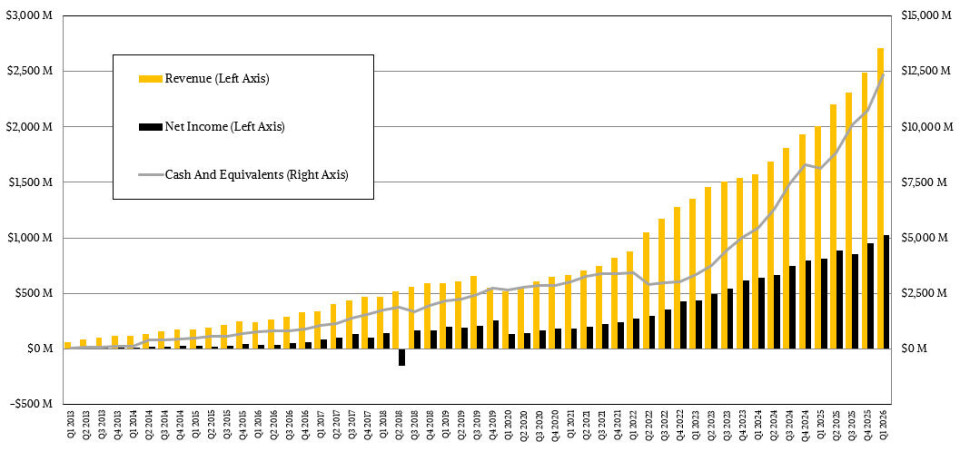

Add

them up and Arista had $2.71 billion in revenues, up 35.1 percent year on year

and up 8.9 percent from Q4 2025. Operating income was $1.16 billion (up 34.8

percent) and net income was $1.02 billion (up 25.7 percent, and representing

37.8 percent of revenues.

Arista

ended the March quarter with $12.35 billion in cash and equivalents, up by 51.6

percent since last year and giving it huge latitude in what it does and does

not do. Including prepaying for components to make sure it has a fair share of

supply.

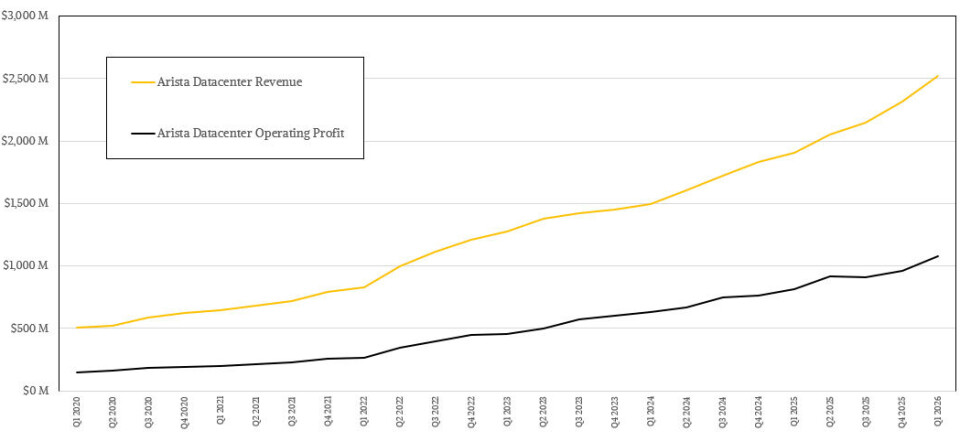

My

model suggests that Arista had $2.52 billion in datacenter revenues in Q1 2026,

up 32.3 percent, with operating income of $1.08 billion, up 32 percent.

It is hard to find a company that is expanding into

new markets and yet keeping an even keel and does it as well as Arista does.