We

live in the future, and sometimes it is just amazing how different things are

today from two decades ago when the age of accelerated computing got its start

in the HPC ModSim arena, eventually being adopted as the architecture of choice

for AI applications.

The

market is utterly transformed, or rather, a new set of infrastructure suppliers

have taken over AI system manufacturing and distribution and the venerable companies

peddling systems of record – IBM, the various parts of Hewlett Packard Enterprise

that started out as Tandem and Digital Equipment, Sun Microsystems – are either

gone or have businesses that are so much smaller relative to a much embiggened

systems market that they do not even rise to the top vendor rankings.

I

have spent some time building this chart below, which shows the sweep of

changes in datacenter compute leading up to the Dot Com boom, when Internet

technologies were first broadly commercialized and when the tremendous amounts

of data to train AI models was first being digitized and amassed. The data is quarterly

server revenues as reckoned by the box counters at IDC, which is the dataset

that has been most broadly available to the public and arguably the most useful

over the decades that IDC gave out summary data to help peddle its deeper market

research and keep its name out there as an IT expert.

During

the rise of GenAI, both IDC and Gartner stopped giving out public data, and the

blue line in the chart shows that gap. IDC recently started giving out quarterly

data, and we have added this to the data set and filled in some gaps with estimates.

We have not adjusted this data for inflation, but probably should. All it would

do is rotate the data around whatever year you picked as the normalized US

dollar. The data to the left of the normalized year would lift further as you

moved to the left into the past, and the data to the right of this

normalization point would be pushed down with increasing vigor as you move to

the right – both due to the effects of inflation.

The

green line shows the peak of server revenues during the Dot Com boom, a level

that in absolute dollars was not reached consistently for two decades. Assuming

the market for systems of record is relatively stable at around somewhere

between $15 billion and $18 billion a quarter– for most back office systems,

Moore’s Law advances plus packaging and networking enhancements offer more

incremental capacity than they could ever dream of using – then the remaining

more than $100 billion in sales of systems are for AI capacity or the front

office and back office systems that feed into them. In that sense, AI is

driving far more than half of the revenues in the server market.

What

is immediately obvious is that if the GenAI bubble bursts, as many worry it

might, there is going to be enough soap for many, many companies to drown in. The

server bust will make the Dot Com Bust, the Great Recession, and other

collapses in the server space look like a joke, as you can plainly see. Nvidia

will be hit the hardest, but many OEMs and ODMs, countless chip suppliers, all

the clouds big and small, up and down the value chain, will take their own

hits.

The

magnitude of such a collapse is hard to grasp. This GenAI boom in its totality

– datacenters and equipment, but also power, cooling, land, and financial vig –

is a significant driver of the global economy, and is largely a phenomenon of

the United States, with China to a less degree (which is odd, but more on that

in a moment) and sovereign nations starting to catch the GenAI religion.

The

good news, if you want to global economy to somehow hold itself together, is

that it looks like demand is well exceeding supply, and the gargantuan AI

projects that have been outlined are still moving ahead.

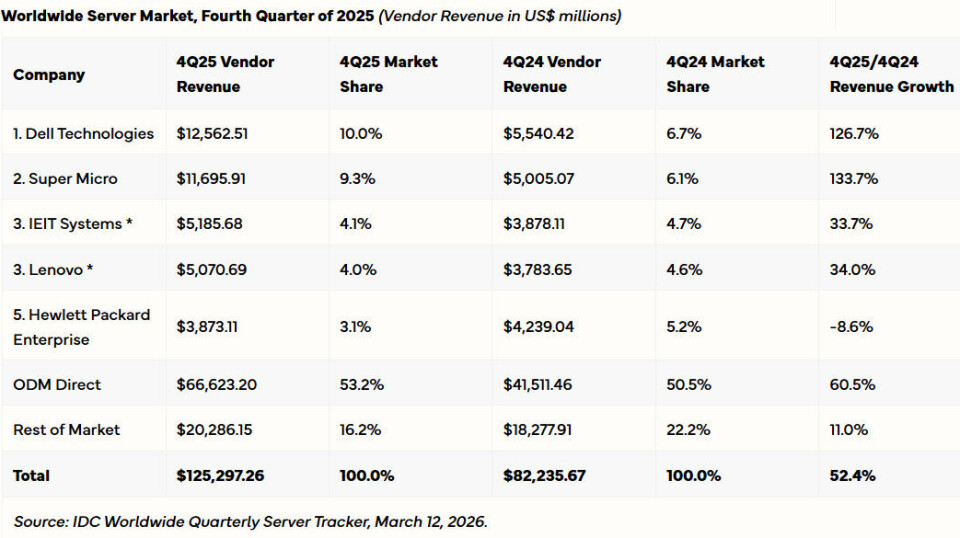

In

the fourth quarter of 2025, the most recent data just released by IDC, server

sales grew by 52.4 percent to $125.3 billion, which also represented an incredible

11.4 percent sequential increase from Q3 2025. Based on what IDC said in its

report, we calculate that of this vast and expensive pile of machinery, $70.65

billion was for GPU-accelerated systems, which represented 56.4 percent of all

server revenues. We do not know how many XPU-accelerated system sales are in

there, but it would have to be a substantial amount. We do not think that IDC

is mixing revenues of systems with GPUs and XPUs, or it would have said as

much. We wish IDC would clarify this because we have a hard time believing

there was $54.65 billion in back office and front office system sales in the

quarter.

What

IDC did say – and which is a distinction that is not all that useful any more, but

you never throw away data – is that X86 CPUs were used in $69.8 billion of

machinery in Q4 2025 (up 16.9 percent year on year) compared to $55.5 billion in

non-X86 servers. While IBM’s Power Systems and System z mainframes are some of

that non-X86 iron, the vast majority by far is now Arm-based servers made by

the hyperscalers, the cloud builders, and now the AI model builders. That was

2.5X growth year on year for the non-X86 camp, and it will not be too long

before the value of machines based on Arm will exceed the value of machines

based on X86.

Mostly

because of the value of the GPUs attached to the Arm systems, but some of it is

indeed Arm-based infrastructure servers that have no accelerators.

Dell

is by far the largest of the server OEMs now, bringing in $12.65 billion in

sales, up by a factor of 2.3X year on year thanks to some large AI system deals.

Supermicro, despite its current difficulties with the

US government over alleged smuggling of sanctioned GPU systems into China, had

a very good Q4, with server sales of $11.7 billion, also up 2.3X year on year.

IEIT Systems, an upstart server maker out of China that is now the number three

OEM in the world, had $5.19 billion in sales, up 33.7 percent. Sino-American

system maker Lenovo, which is ranked number four, had $5.07 billion in server revenues,

up 34 percent, while HPE, which is getting more and more picky about deals

because it doesn’t want to take lower margins on AI deals, had $3.87 billion in

sales, down 8.6 percent year on year but up 14 percent sequentially.

Other

OEMs comprised $20.29 billion in server revenues in Q4 2025, up 11 percent as a

group, while the ODMs – Foxconn, Inventec, Quanta, WiWynn, Jabil, and others –

as a group shipped $66.62 billion in server gear, down a smidgen sequentially

but up 60.5 percent year on year.

Which

brings us to the geopolitical part of servers.

“The

United States is the fastest growing region in the server market, with an

increase of 72.4 percent compared to the fourth quarter of 2024, fueled by 80.1

percent growth in the accelerated server segment,” IDC wrote in its report. “Canada

grew 70.7 percent, pushed by the same reason. EMEA and APeJC also showed double

digit growth, with 43.6 percent and 27.9 percent, respectively. PRC and Latin

America showed smoother but healthy growth of 17.7 percent and 12.8 percent

each while Japan declined by 4.7 percent as it couldn’t match an important

investment a year ago.”

What IDC doesn’t tell us is what the server spending

amounts are by country, but clearly China is now growing its server budgets

anywhere near the rate that we are seeing among the tech titans in the United

States. This seems perplexing to us. If China is so much smarter about AI, as

many contend it is and

as

the DeepSeek model first demonstrated back in January 2025

, then maybe the

total addressable market in China is not as big as we might be led to believe.